Lower Oil Prices: An Opportunity for Oil and Gas Companies

Article reproduced with the permission of Geopolitical Information Service.

The global drop in oil prices has analysts mulling over the shrinking profitability of the oil industry. But it is not all doom and gloom. On the contrary, companies may be in a stronger position today to negotiate better deals with host governments, compared with when prices were high.

Oil prices are the most obvious drivers of change in the relationship between the two key players: host governments – the owners of resources; and companies – the holders of capital and technology. The price level significantly determines the degree of bargaining power each party has at the negotiating table. Typically, when the oil price is high, the government has the upper hand; when the price moves in the opposite direction, the pendulum swings in favour of the companies. Even before the oil price started to weaken, some governments introduced drastic changes to improve their investment outlook. Such moves further toughen competition between countries for international capital. It is, however, a question of time before the pendulum swings again.

The world's media has been highlighting the detrimental effects the fall in the oil price has had on the oil industry. This is not surprising since lower oil prices mean shrinking profitability, everything else being equal.

But high oil prices are not always accompanied by higher profits, just as a fall in the price does not necessarily bring doom and gloom to this more-than-a-century-old industry.

Oil prices are the most obvious drivers of change in the relationship between the two key players: host governments – the owners of resources; and companies – the holders of capital and technology. Both players want to maximise revenues from the same source: the oil and gas sector. Tensions will therefore always exist.

Bargaining power

The price plays a significant role in determining the degree of bargaining power each party has at the negotiating table. Typically, when the oil price is high, the government has the upper hand; when the price moves in the opposite direction, the pendulum swings in favour of the companies.

Crude oil prices are down almost 50 per cent since 2014. This considerable drop is not without precedent. In 1986, the price fell by around 48 per cent; in 1998 by some 33 per cent and in 2009 by 37 per cent from previous highs.

In the first case, what followed was several years of lowish prices with new investment shrivelling in oil and gas, alternatives were abandoned, and an era of cheap energy was taken for granted.

In the second case, after a short period, there was continuous price escalation with the oil price reaching a record high of US$145 per barrel (/bl); a few months later, oil was trading at nearly US$30/bl. Between 2011 and mid-2014, oil prices achieved an unusual stability hovering above US$100/bl.

Disruptions to supply

As additional oil supplies, mainly driven by US shale, maintained their growth momentum, which more than compensated for existing disruptions to supply, the oil price fell again and has been varying between US$50 and $60 ever since.

The immediate reaction of companies – from explorers and producers to service providers – is to cut down on spending. Low yielding projects have been shelved, others deferred. It has been reported that projects worth US$200 billion have been cancelled within the last three months alone. Companies have also announced plans to lay off more than 100,000 workers worldwide.

BP's CEO, Bob Dudley, described this new diet as "resetting" the company, "managing and rebalancing our capital programme and cost base for the new reality of lower prices". By the same token, Saudi Aramco's CEO, Khalid Al Falih was reported saying, "Like everyone else, we are using the downturn as an opportunity to sharpen our fiscal discipline."

High prices

Experience shows that periods of high oil prices are not always good news for the industry. On the contrary; they typically attract higher taxes, contract renegotiations, tougher regulations and, in extreme cases, expropriation and nationalisation as host governments demand a bigger share of the additional returns.

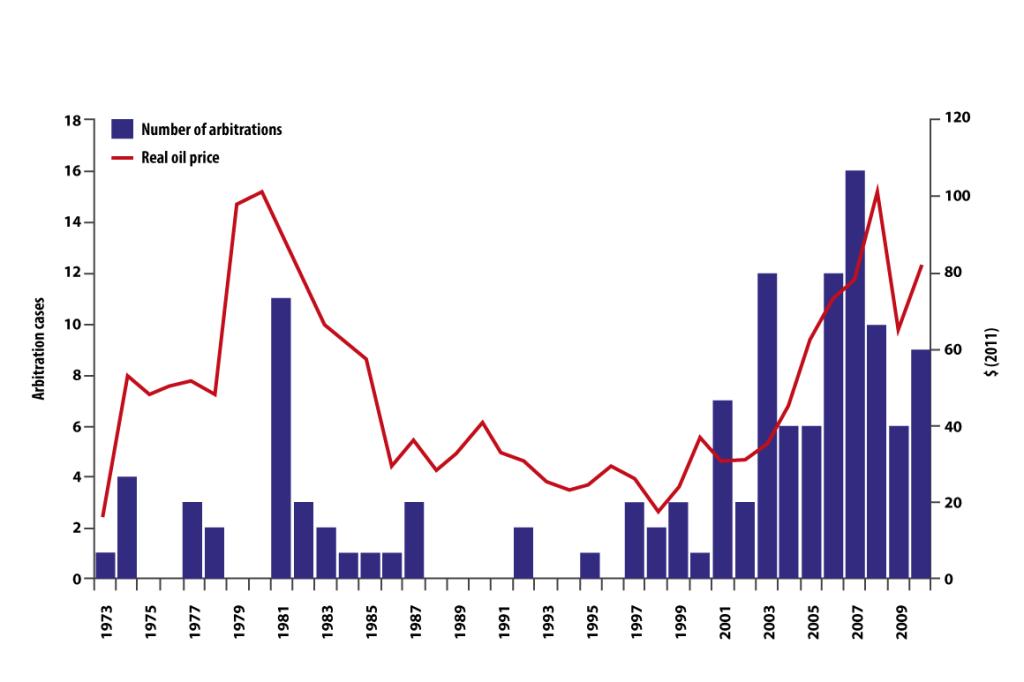

These changes are seldom implemented easily or peacefully, and often result in lengthy litigation. As shown by London-based think tank Chatham House, the higher incidence of arbitrations in the oil sector correlates strongly with the commodity price boom. A contract signed when oil prices were US$30/bl may well be viewed as simply too generous to the industry at US$100/bl.

Oil prices and international arbitration cases, 1973–2010 (Chatham House, 2013)

The period between 2002 and 2008 is a good illustration. Over that period, oil prices were rising steadily and more than 30 countries revised their petroleum taxation systems to increase their share of profits.

From Angola to Argentina, China, Ecuador, India, Kazakhstan, Libya, Nigeria, US (Alaska), governments increased the tax rates oil companies pay.

Petroleum law

Countries like Algeria modified their petroleum legislation law in order to give a minimum equity share to their national oil company, Sonatrach. In an extreme case, Venezuela replaced all the then-existing terms with new contracts and imposed a majority equity share for its national company, PDVSA. The late Venezuelan president, Hugo Chavez, confronted the industry with an "accept it or leave it" offer. Companies like ExxonMobil resorted to the international arbitration court to resolve the matter.

As The Economist outlined in a March 2007 article, "All around the world, from Algeria to China, governments are changing the terms of investment in oil and gas, on the ground that they are not receiving their fair share of the profits. For critics of capitalism, last year's surge in oil and gas prices seemed to present a long-awaited chance to shift the global balance of power away from corporate behemoths and the governments that are closest to them."

Attract investment

Today's low oil prices have pushed some governments to go in the opposite direction. This is most notable in countries which have been struggling to increase production and attract investment. Low oil prices will only exacerbate an already dire situation and therefore prompt anxious governments to implement drastic measures to stop conditions from worsening further.

For instance, energy giant BP and its oil and gas partner, RWE Dea, recently made headlines after signing a historic deal with the Egyptian government. The contract has been described by some critics as the "great Egyptian gas giveaway". While such a statement is surely an exaggeration, it indicates the Egyptian authorities' willingness to try different means, even completely new schemes, to improve the country's challenging investment outlook. The agreement shifts away from a production-sharing model – long used by Egypt whereby companies are paid a share of production as a compensation for their efforts – to a concessionary system where the companies own all the production and pay taxes in return.

Privatising industry

Some equate this system, which is dominant in the Organisation for Economic Cooperation and Development (OECD), to privatising the industry, wrongly in the author's view, but the BP deal surely reflects a more accommodating government attitude.

In the UK, where the North Sea has been hit hard by falling oil prices, the chancellor, George Osborne, announced in his March 2015 budget a US$1.9 billion support package to the industry, including a reduction in the tax burden and the provision of additional support for exploration of the UK Continental Shelf (UKCS).

Even before the oil price started to weaken, some governments introduced drastic changes to improve the investment conditions in their oil and gas sectors. Such moves toughen competition between countries for private capital.

Hoping to rescue the economy by stimulating interest in new energy developments, the Algerian government revised its hydrocarbon law in 2013, providing tax incentives and relaxing some of the sector's otherwise strict regulations.

During the same year, Mexico modified its constitution which, for 75 years, prohibited private investment in the oil sector. This U-turn policy ends the monopoly of the state oil company, Pemex.

Energy reform

Iran also embarked on a radical energy reform. In February 2014, the country announced the introduction of new contracts and fiscal arrangements for upstream oil and gas to attract foreign capital and technology for exploration and production ventures. The new arrangement known as the Iran Petroleum Contract (IPC) will cover a period of 20 years compared with the existing short term agreements of less than 10 years, which were not favoured by the oil companies.

The longer the oil prices stay low, the longer this list will become as the industry implements a strict spending discipline and prioritises the allocation of its limited resources.

The relationship between the oil industry and host governments has been best described as a swinging pendulum, mainly pushed by the oil price.

The industry looks like it is having a tough time. But the longer the oil price remains low, the more likely companies are to sign attractive deals with host governments. The danger, however, is agreeing generous terms because it is those contracts that risk being revised first when the oil price starts to rise again.

Confidence in global energy market

- According to a DNV survey, given the fall in oil prices, just 28% of respondents are confident about the oil and gas industry, sharply down from 88% in 2014, and a high of 89% in 2013

- Shell, the Anglo-Dutch oil major, abandoned plans for one of the world's biggest petrochemical plants, a US$6.5bn project with Qatar Petroleum – the Al Karaana project

- Norwegian Statoil handed back three exploration licences on the west coast of Greenland and postponed work on its Corner field project in Alberta for at least three years

- French Total announced that its capital spending in 2017 will be 11% below 2013's peak

- China Sinopec announced it will cut its 2015 capital expenditure by 12.1%, to US$21.9 bn

- Between 2001 and 2010, arbitration cases for oil/gas increased more than tenfold compared with previous decade

- The World Bank's International Centre for Settlement of Investment Disputes (ICSID) decided unanimously in October 2014 that Venezuela had to pay US$1.6bn damages to ExxonMobil for assets taken by state-owned PDVSA in 2007

- The UK government reduced the headline tax rates for oil and gas fields down from the current 60% to 50% and 81% to 67.5% for mature fields

Dr. Carole Nakhle is director of Crystol Energy, UK. She is an energy economist who has worked in academia, the oil and gas industry, and policymaking, and as a consultant to the IMF, World Bank and Commonwealth Secretariat.

Dr. Nakhle will be among experts from around the world to discuss these issues at the forthcoming NRGI conference on 25 and 26 June in Oxford.